|

First, the market review

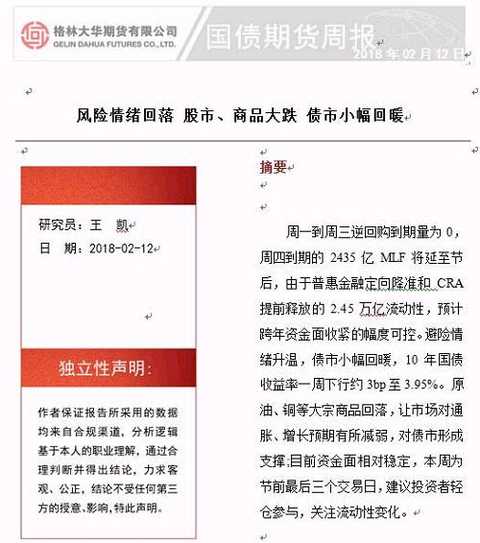

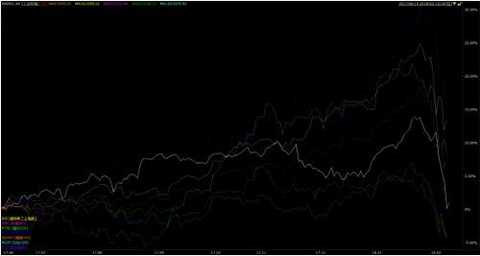

Figure 1 T1806 trend last week

|

Source: Greenwich Futures Research Institute, Wenhua Finance

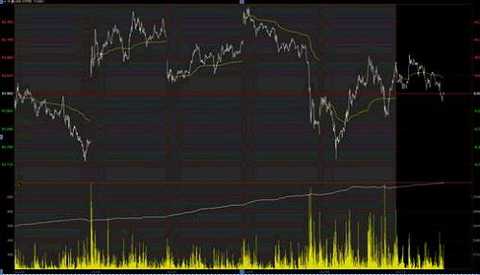

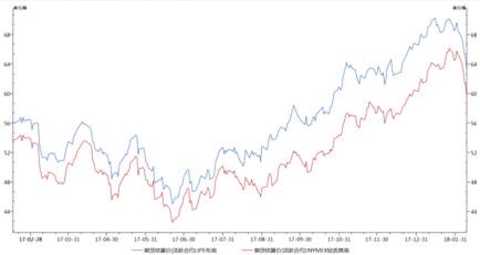

Figure 2 TF1806 recent trend

|

Source: Greenwich Futures Research Institute, Wenhua Finance

Last week, the funds were loose, global stock markets plummeted, commodity prices fell back, market risk appetite fell, and the bond market rebounded slightly. Treasury yields generally declined. Among them, 5-year Treasury yields were down 1.59 bp, 10-year Treasury yields were only 3.17 bp, and ultra-short-term varieties were down. The weekly treasury futures fluctuated widely, with TF1806 up 0.07% and T1806 up 0.08%. Shift led the main contract position to 1806 contract, T1806 Masukura 9611 hands, TF1806 Masukura 6564 hands.

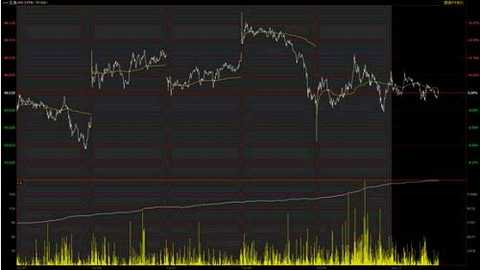

Figure 3 Main term structure

|

Source: Greenwich Futures Research Institute, WIND

Second, the analysis of influencing factors

1. Global stock market suffered a setback

Figure 4 Global major stock index trend

|

Source: Wind, Greenwich Futures Research Institute

National stock markets have suffered a "blood wash." The Dow Jones index fell 5.2% in a single week, and the VIX index soared to 50 (close to the high point formed by the RMB exchange rate reform in August 2015); domestic A shares also fell 9.6%, the biggest drop since August 2015.

Figure 5 Brent and WTI oil price trend

|

Source: Wind, Greenwich Futures Research Institute

Major commodities such as crude oil and copper showed significant corrections. Both WTI and cloth oil fell by more than 8%, and copper prices fell by nearly 5%.

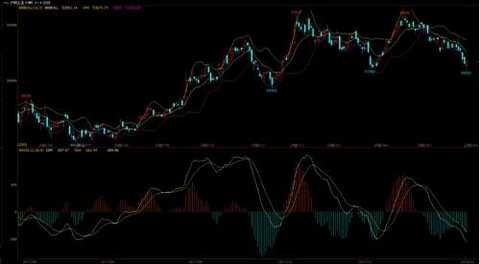

Figure 6 Shanghai copper main trend

|

Source: Wenhua Finance

2. Capital stability

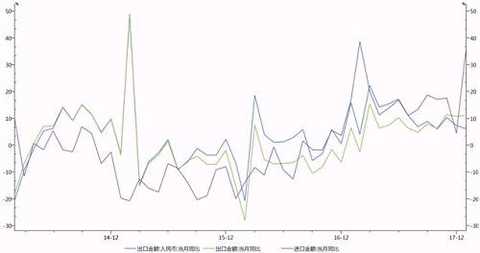

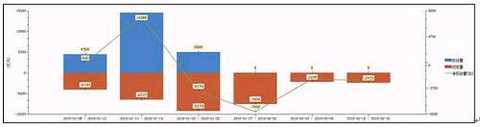

Figure 7: Year-on-year growth rate of import and export

|

Source: Wind, Greenwich Futures Research Institute

January imports were 36.9% year-on-year (in US dollars), expected to be 10.8%, the previous value was 4.5%; China's January exports were in January (in US dollars) 11.1%, expected to be 10.8%, the previous value was 10.9%; January imports year-on-year (in RMB) 30.2%, expected 5.3%, the previous value of 0.9%; 1 China's January exports in January (in RMB) 6%, expected 2.6%, the previous value of 7.4%.

The renminbi has entered an appreciation cycle. Under this circumstance, the dollar-denominated import and export growth rate is higher than the renminbi-denominated import and export growth rate: January exports were 5.1% higher and imports were 6.7% higher. For export manufacturers, the cost side is mostly renminbi-denominated, so when analyzing exports, renminbi-denominated exports can better reflect the company's export revenue. Under the condition of continued appreciation of the renminbi, imports have a price advantage, causing domestic demand to spill abroad.

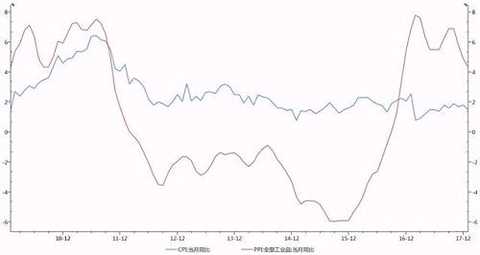

Food prices rose by 2.2% month-on-month, and about 0.4% of CPI (more than 2/3 contribution). Among them, the cold weather caused the price of fresh vegetables to rise, which affected the CPI upwards by 0.33%. And this increase is mainly driven by seasonality.

Non-food prices are still stabilizing, and it is difficult for the inflation center to continue to rise. Non-food CPI was 0.2%, up 2.0% year-on-year. The price is still stable. The NDRC continuously raised oil prices at the end of December, mid-January and late January, pushing up the growth rate of transportation fuels. Excluding the impact of oil prices, non-food inflation has a smaller upward trend. This reflects the fact that the non-food inflation center is unlikely to continue to rise in the context of a moderate economic recovery.

The PPI is slower than the fall. The January PPI was 0.3%, compared with 4.3%. From the perspective of the growth rate of the ring, the PPI is slower. In the future, we need to pay attention to two points: First, the price of the processing industry in the processing industry has dropped to zero, and the weight of the processing industry in the PPI has accounted for about 45%. The rapid decline in the price indicates that the PPI may accelerate its decline in the future. Second, the price of living materials continued to decline, only 0.1% from the previous month and down to 0.3% year-on-year. The signs of PPI conduction to CPI are not obvious.

Figure 8 CPI, PPI year-on-year growth rate

|

Source: Wind, Greenwich Futures Research Institute

3. The funds face remain stable

Figure 9 Recent central bank open market operations

|

Source: Wind, Greenwich Futures Research Institute

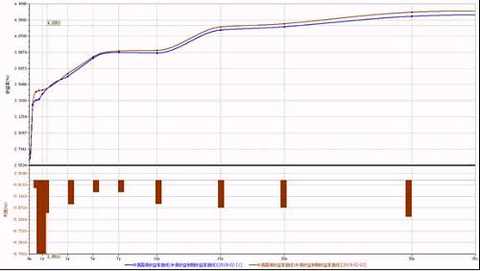

Figure 10 Currency scale and expiration date this week

| name | Issue/expiration | Date of occurrence | Issuance (100 million yuan) | interest rate(%) | Term (month) | Term (days) | Value date | Date of Expiry |

| MLF365D | MLF (return) | 2018-02-15 | 2,435.00 | 3.1000 | 12 | 365 | 2017-02-15 | 2018-02-15 |

| Treasury is kept for 3 months | Treasury cash deposits due | 2018-02-23 | 1,200.00 | 4.6000 | 3 | 98 | 2017-11-17 | 2018-02-23 |

Source: Wind, Greenwich Futures Research Institute

Last week, the central bank returned to buy 220 billion yuan, and the state treasury will release 100 billion yuan of liquidity. This week, the funds are still relatively loose. In addition to the small amount of maturity, it also benefits mainly from two points: First, the central bank's inclusive financial downgrades release long-term liquidity of about 450 billion; the second is a 30-day temporary preparation. The Gold Use Arrangement (CRA) has released a total of nearly 2 trillion temporary liquidity.

The main factor affecting liquidity this week is cash demand. The reverse repurchase maturity is 0 from Monday to Wednesday, and the 243.5 billion MLF due on Thursday will be postponed to the end of the holiday period, so the overall maturity of this week is 0. As the Spring Festival approaches, cash withdrawals will rise significantly and become a major factor affecting liquidity this week. On the whole, with the rise in cash demand, the funding side may be marginally tightened. However, due to the targeted reduction of Pratt & Whitney and the 2.45 trillion liquidity released by CRA in advance, it is expected that the tightening of funds across the years will be controllable.

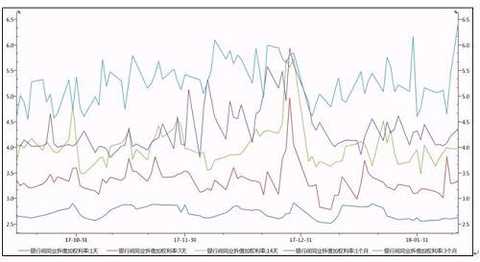

Figure 11 Interbank lending weighted interest rate

|

Source: Greenwich Futures Research Institute, WIND

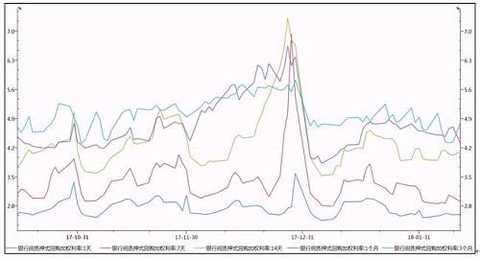

Figure 12 Interbank pledged repo weighted interest rate

|

Source: Greenwich Futures Research Institute, WIND

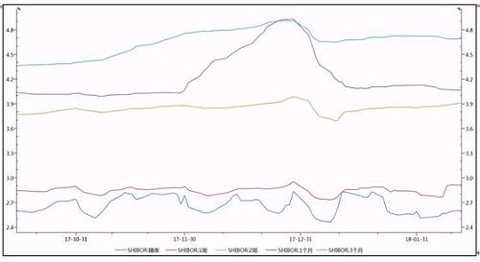

Figure 13 Shanghai Interbank Offered Rate (SHIBOR)

|

Source: Greenwich Futures Research Institute, WIND

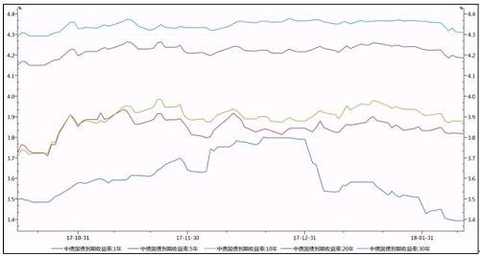

In the near term, the funds were stable, which was better than the same period before the Spring Festival in previous years . In one year, short-term government bonds fell sharply, and the spread between 10- year and 1- year government bonds expanded to around 90 BP .

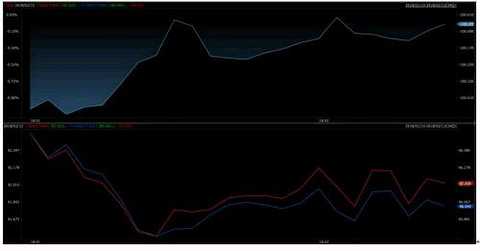

Figure 14 Yield of maturity of different maturity bonds

|

Source: Greenwich Futures Research Institute, WIND

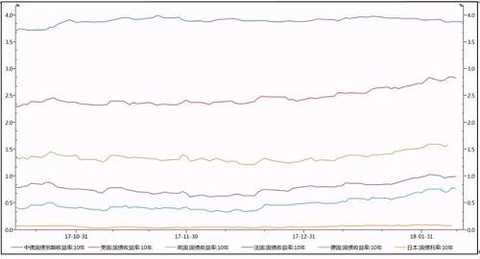

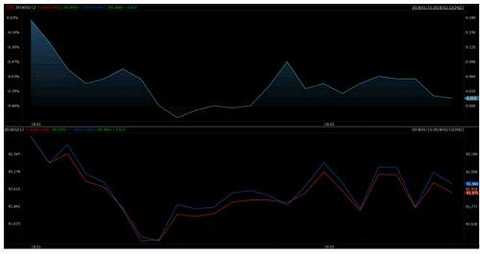

Figure 15 Trends in 10-year Treasury yields in major economies

|

Source: Greenwich Futures Research Institute, WIND

In the 10- year period, the US bond spread narrowed rapidly. Since the high of 1.665 in 2017, it has fallen back to around 1.000, and the cumulative downside is over 60bp.

Figure 16 Trends in the 10-year bond and US bond spreads

|

Source: Greenwich Futures Research Institute, WIND

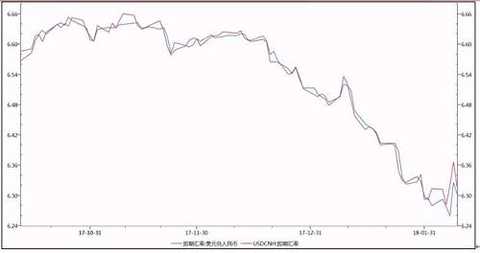

Figure 17 USD/RMB spot exchange rate trend

|

Source: Greenwich Futures Research Institute, WIND

The renminbi has been sharply adjusted. The renminbi that had been triumphantly ushered in a "retaliatory" callback on Thursday, the US dollar index rebounded nearly 1.5% a week, and the renminbi against the US dollar fluctuated greatly and depreciated slightly.

2. Analysis of arbitrage of national debt futures

2.1 Cross-species arbitrage

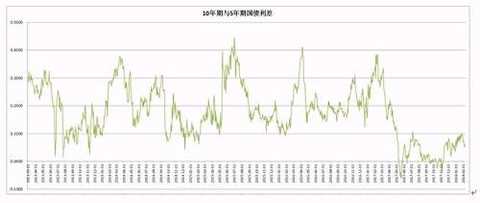

The 10- year and 5-year government bond spreads rebounded slightly, but remained at a relatively low level.

Figure 18 Trends in 10-year and 5-year government bond spreads

|

Source: Greenwich Futures Research Institute, WIND

Figure 19 Analysis of the price difference between 1 and 1 hand T1806 and 2 hands TF1803

|

Source: Wind, Greenwich Futures Research Institute

2.2 Intertemporal arbitrage

Figure 20 Analysis of the trend of the spread between multiple T1806 and empty T1803

|

Source: Greenwich Futures Research Institute, WIND

Third, the market pre-judgment

The repurchase maturity is 0 from Monday to Wednesday, and the 243.5 billion MLF due on Thursday will be postponed after the holiday. Due to the targeted reduction of Pratt & Whitney and the 2.45 trillion liquidity released by CRA in advance, the inter-annual funding is expected to tighten. The magnitude is controllable. The risk aversion has warmed up, and the bond market has rebounded slightly. The 10-year government bond yield has dropped by about 3bp to 3.95% a week. Crude oil, copper and other commodities fell, allowing the market to weaken inflation and growth expectations, and support the bond market; the current funding is relatively stable, this week is the last three trading days before the holiday, investors are recommended to participate in light warehouse, pay attention Changes in liquidity.

Important statement

The information in this report is based on publicly available information. We do not guarantee the accuracy or completeness of this information. We do not guarantee that the information has been changed in the latest information, nor does it guarantee that any changes made by the analyst will not change. In any event, the information in the report or the opinions expressed do not constitute a bid or inquiry for the sale or purchase of the futures product. Under no circumstances will our company make any form of guarantee for any investment in any of the contents of this report, and investors will invest in it and the investment risk will be borne by itself. Our company may issue other reports that are inconsistent with the opinions of this report. This report reflects the opinions and conclusions of the company's analysts and does not represent the position of our company. Without the consent of our company, no one may publish, reproduce or revise or modify this report in any way.

(Editor: Shao Yidi HF116)

[Disclaimer] This article only represents the views of the cooperating contributors and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

Anti Satic Fabric,Anti Static Stripe Fabric,Conductive Anti Static Fabric,Proof Anti Static Fabric

Shaoxing Yingcheng Textile Co.,Ltd , https://www.sxyingcheng.com